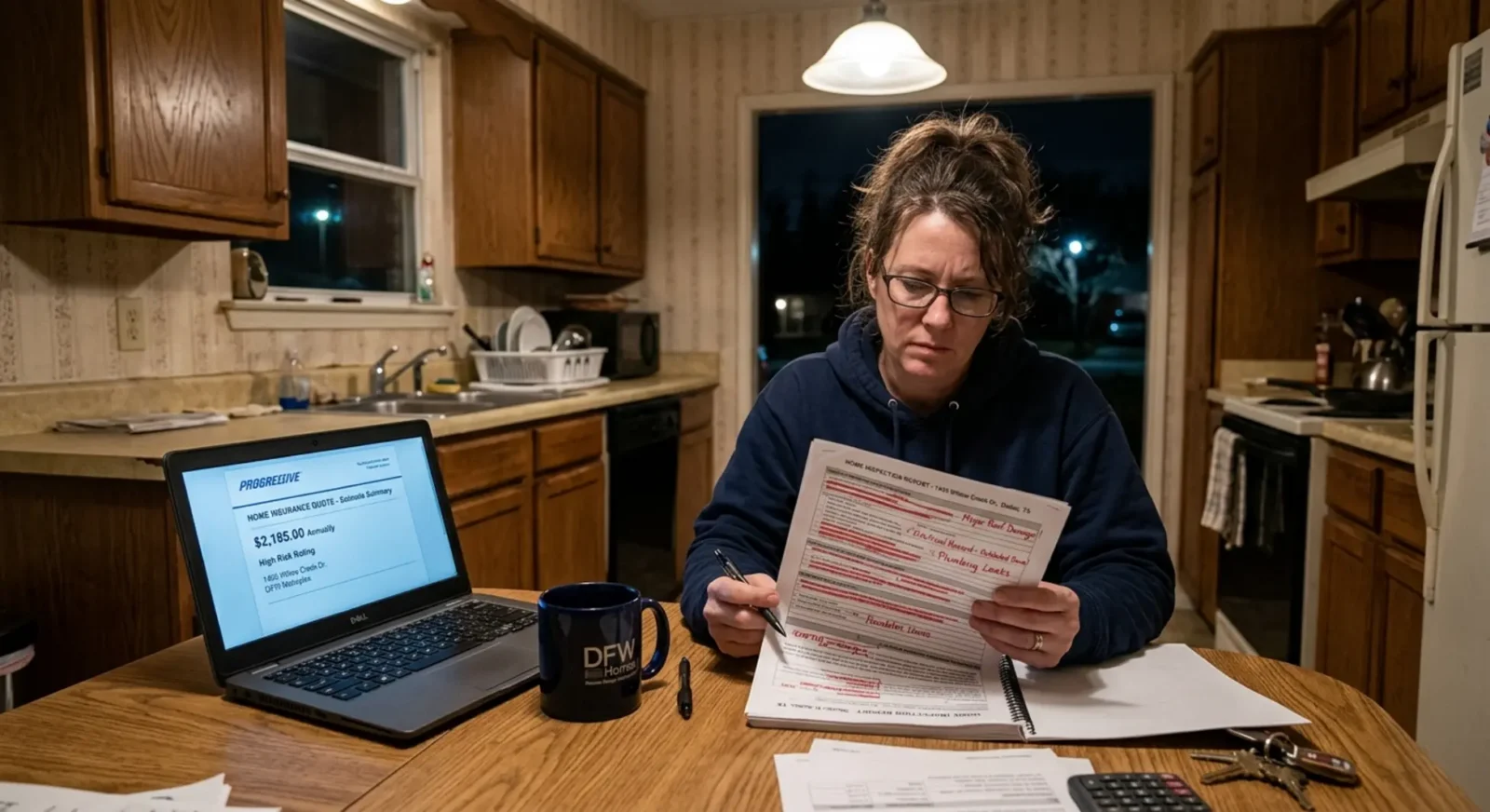

Six months after closing on a home in the Fort Worth suburbs, a buyer gets a call from a foundation repair company. The estimate: $28,000. The cause: significant slab movement from DFW’s notorious clay soil — movement that was visible, documentable, and should have been flagged during the pre-purchase inspection. The inspector’s report said the foundation was “functional.” The inspector carried no Errors & Omissions insurance. The buyer had no recourse. The $28,000 came out of their savings.

This is exactly why understanding property inspector liability insurance and professional standards matters — not as abstract regulatory trivia, but as real financial protection for one of the largest purchases you’ll ever make. When you hire a home inspector, you’re not just paying for a report. You’re paying for professional accountability. And in Texas, that accountability is only as strong as the inspector’s licensing, insurance coverage, and commitment to professional standards.

This guide breaks down everything DFW homebuyers need to know: what E&O insurance actually covers, how TREC licensing works, what professional certifications signal, and how to spot inspectors who cut corners on the protections that matter most. Whether you’re buying your first home in Weatherford or your fifth in Southlake, this information will help you hire with confidence.

Key Takeaways

- E&O insurance is your financial safety net if an inspector negligently misses significant defects — but coverage limits and contract liability caps determine how much you can actually recover.

- TREC licensing is mandatory in Texas — and there’s a meaningful difference between a Professional Real Estate Inspector (PREI) and a basic Real Estate Inspector (REI).

- Professional certifications from ASHI or InterNACHI signal a commitment to quality that goes well beyond state minimum requirements.

- Always verify insurance and license status before signing an inspection agreement — reputable inspectors provide proof without hesitation.

- Saving $200–$300 on an uninsured inspector can expose you to $10,000–$50,000+ in uncovered repair costs if major defects are missed.

- DFW’s clay soil and slab foundations create inspection challenges that require local expertise — not just a generic checklist.

- The DFW market has 1,000–1,500+ licensed inspectors — choice is good, but evaluating quality carefully is essential.

Why Property Inspector Liability Insurance Matters for Homebuyers

Most homebuyers think of a home inspection as a formality — a box to check before closing. But a home inspection is actually a professional service with legal and financial implications. When an inspector misses a significant defect due to negligence, the question isn’t just “who fixes it?” — it’s “who pays for it?” That answer depends almost entirely on whether your inspector carries adequate liability insurance.

The professional home inspection services provided by licensed, insured inspectors include more than a written report. They include the professional accountability that comes with Errors & Omissions (E&O) insurance — a policy specifically designed to cover financial losses when an inspector’s negligence causes harm. Without it, you have a report but no recourse.

According to insurance industry data, defense costs alone for inspection liability claims can reach $5,000–$15,000 before any settlement is reached. Payouts for significant missed defects — foundation issues, major roof failures, hidden plumbing leaks — routinely range from $10,000 to $50,000 or more. These aren’t edge cases. They’re the exact scenarios E&O insurance exists to address.

The Real Cost of Missed Defects in the DFW Market

DFW’s housing market creates specific conditions that make thorough inspections — and the insurance backing them — especially critical. The region’s expansive clay soil is one of the most significant factors. As soil moisture fluctuates through Texas’s hot, dry summers and wet winters, slab foundations shift. This movement is gradual, often invisible to an untrained eye, and can cost $10,000–$50,000+ to repair once it becomes a structural problem.

Roof defects are another major category. North Texas hailstorms are frequent and severe, and damaged roofing that goes undetected during an inspection becomes the buyer’s problem after closing. A full roof replacement in DFW runs $8,000–$20,000 depending on home size and materials. HVAC systems stressed by extreme summer heat can fail within months of purchase if underlying issues aren’t caught. Plumbing leaks hidden behind finished walls can cause mold growth that costs far more to remediate than the original leak.

The math is straightforward: the difference between hiring an inspector who charges $500 and one who charges $350 is $150. The difference between an inspector who carries adequate E&O coverage and one who doesn’t could be $30,000 out of your pocket. That’s not a hypothetical — it’s a documented pattern in inspection liability cases across Texas.

How E&O Insurance Protects You as a Buyer

E&O insurance works by covering the inspector’s legal defense costs and any settlement or judgment that results from a successful negligence claim. If an inspector misses a defect that a reasonably competent professional should have caught, and that defect causes you financial harm, E&O insurance is the mechanism that makes you whole — up to the policy limits.

Coverage limits vary significantly. TREC requires a minimum of $100,000 per occurrence and $500,000 aggregate for Professional Real Estate Inspectors. Higher-quality inspectors and larger firms often carry $500,000 to $1,000,000+ in coverage. The difference matters: a $100,000 policy may be exhausted by legal defense costs alone before any settlement is paid. A $500,000 or $1,000,000 policy provides substantially stronger protection.

It’s also worth understanding what E&O insurance doesn’t cover. It doesn’t cover defects that were genuinely hidden or undetectable. It doesn’t cover cosmetic issues or items outside the TREC Standards of Practice scope. And critically, it doesn’t override liability caps in the inspection contract — a point we’ll address in detail shortly.

⚠️ The Hidden Cost of Uninsured Inspectors

Hiring an uninsured inspector to save $200–$300 exposes you to $10,000–$50,000+ in repair costs if major defects are missed. A single foundation issue or roof problem can cost far more than the inspection fee savings — and without E&O coverage, your only option is costly, time-consuming legal action against an individual who may have no assets to pursue.

Understanding Errors & Omissions (E&O) Insurance for Home Inspectors

E&O insurance is a form of professional liability coverage specifically designed for service professionals whose work product — in this case, an inspection report — can cause financial harm if it contains errors or omissions. For home inspectors, it’s the primary financial protection mechanism available to buyers when things go wrong.

Understanding the TREC licensing requirements around E&O insurance helps clarify what you’re entitled to expect. TREC Rule 531.18 mandates that Professional Real Estate Inspectors (PREIs) carry a minimum of $100,000 per occurrence and $500,000 aggregate in E&O coverage. This is a floor, not a ceiling — and for many DFW properties, it’s a relatively low floor given the cost of potential repairs.

E&O premiums for Texas home inspectors range from $1,500 to $5,000+ annually for solo operators, and significantly more for multi-inspector firms. In the DFW market specifically, premiums tend to run higher than the national average — roughly $2,000–$4,000 annually — due to the competitive market, claim frequency, and the complexity of DFW-specific inspection challenges like slab foundations and clay soil. These costs are built into inspection pricing, which is one reason why a fully insured inspector charges more than an uninsured one.

Coverage Limits and What They Mean for Your Protection

The difference between a $100,000 E&O policy and a $1,000,000 policy isn’t just a number — it’s the difference between meaningful protection and a policy that gets consumed by legal fees before you see a dollar of recovery.

Here’s how it works in practice: if you file a claim against an inspector for a missed foundation defect requiring $35,000 in repairs, the insurance company will investigate, potentially hire experts, and provide legal defense for the inspector. Defense costs alone can run $10,000–$20,000. If the policy limit is $100,000, there’s room for a reasonable settlement. But if the inspector has multiple claims in a policy year, the aggregate limit matters — once the aggregate is exhausted, no further claims are paid from that policy period.

When evaluating inspectors, ask specifically about their per-occurrence and aggregate limits. A $500,000 per-occurrence limit is a reasonable target for DFW properties. $1,000,000 or higher is even better, and is typical of larger firms and national franchises. Always request a current certificate of insurance — not just a verbal confirmation — showing the carrier name, policy dates, and coverage amounts.

Policy Exclusions and Liability Caps: The Fine Print That Matters

Here’s a reality that many buyers don’t discover until it’s too late: even if an inspector carries adequate E&O insurance, the inspection contract itself may cap your maximum recovery at the inspection fee paid. This is a standard clause in many Texas inspection agreements. If you paid $500 for the inspection, the contract may limit your total recovery to $500 — regardless of the inspector’s insurance policy limits.

This doesn’t mean E&O insurance is useless — it means you need to read the contract carefully before signing. Some inspectors use more buyer-friendly contract language. Others use aggressive liability caps. Understanding what you’re agreeing to before the inspection happens is the only way to know your actual exposure.

E&O policies also contain exclusions. Common exclusions include defects that were genuinely concealed (behind finished walls, underground), issues that fall outside TREC’s Standards of Practice scope, and intentional misconduct. The policy covers negligence — failing to identify what a reasonably competent inspector should have found — not every possible scenario where something goes wrong after closing.

Request a copy of the inspection agreement before booking. Read the liability limitation clauses. If the contract caps your recovery at the inspection fee, that’s important information to factor into your hiring decision. Inspectors who offer more balanced contract terms are demonstrating confidence in their work.

💡 Pro Tip: Ask for Proof of Insurance Before Booking

Don’t just take an inspector’s word that they carry E&O insurance. Request a copy of their current insurance certificate showing coverage limits, policy dates, and carrier information. Reputable inspectors will provide this without hesitation. If an inspector is vague about coverage details or reluctant to share documentation, treat that as a significant red flag.

If you’re looking for an inspector who carries comprehensive E&O and General Liability insurance with transparent coverage details, that’s exactly what properly credentialed inspection firms are designed to provide. Journey Home Inspections maintains robust coverage and will share documentation upfront.

TREC Licensing: The Foundation of Professional Standards in Texas

In Texas, home inspectors are licensed and regulated by the Texas Real Estate Commission (TREC). Operating as a home inspector without a TREC license is illegal — a fact that’s worth emphasizing because unlicensed inspectors do exist, often advertising low prices to attract cost-conscious buyers. If you hire one, you have essentially no legal recourse when something goes wrong.

TREC issues two types of inspector licenses, and the difference between them matters significantly for buyers. Understanding which type of license your inspector holds — and what that means for their experience and independence — is one of the most important steps in the hiring process. You can verify an inspector’s TREC license status directly through TREC’s official license search tool, which is free and takes about two minutes.

For a deeper dive into the full licensing framework, the Texas home inspector license requirements and certification guide covers the complete education, experience, and examination pathway in detail.

PREI vs. REI: Which License Type Should You Hire?

A Professional Real Estate Inspector (PREI) is the higher of the two license designations. To earn a PREI license, an inspector must complete 360 hours of qualifying education, accumulate 4 years of experience as a licensed Real Estate Inspector, pass the TREC Real Estate Inspector examination, and maintain 16 hours of continuing education annually. PREIs can work independently and can supervise other inspectors.

A Real Estate Inspector (REI) has completed basic education requirements and passed the licensing exam, but has less experience and must work under the supervision of a PREI. REIs are not permitted to practice independently. While REIs can be capable inspectors — especially when working under strong supervision — the PREI designation represents a meaningfully higher standard of experience and accountability.

For complex DFW properties — older homes with aging systems, properties on problematic clay soil, homes with additions or non-standard construction — hiring a PREI is the safer choice. The additional experience requirement isn’t just a bureaucratic hurdle; it represents years of real-world inspection experience that directly translates to better defect identification.

When you use TREC’s license search tool, you’ll see the license type listed alongside the inspector’s name. Look for “Active” status and confirm whether the designation is PREI or REI. Also check for any disciplinary actions — TREC publishes enforcement actions publicly, and a history of violations is a serious red flag.

TREC Standards of Practice: What Inspectors Must — and Aren’t Required to — Do

TREC Rule 535.227 establishes the Standards of Practice (SOP) that define the minimum scope of a Texas home inspection. Understanding the SOP helps buyers set realistic expectations and understand the limits of what an inspection can and cannot reveal.

Under the SOP, inspectors must evaluate all major systems: structural components, electrical systems, plumbing systems, HVAC systems, roofing, insulation and ventilation, interior and exterior components, and built-in appliances. The inspection must be visual — inspectors observe accessible components and report on their condition at the time of inspection.

What the SOP does not require is equally important to understand. Inspectors are not required to enter areas that are unsafe or inaccessible. They are not required to inspect below-grade areas (underground), behind finished wall surfaces, or inside walls. They are not required to operate systems under conditions that could cause damage (for example, running an air conditioner when outdoor temperatures are below 60°F). They are not required to report on cosmetic issues, code compliance (unless specifically contracted), or the projected life expectancy of components.

This means a thorough inspection can still miss defects that are genuinely hidden — and that’s not necessarily negligence. The distinction between a defect that was reasonably discoverable and one that was genuinely concealed is central to any E&O insurance claim. Understanding this distinction helps buyers approach inspections with appropriate expectations while still holding inspectors accountable for what they should have found.

📋 PREI vs. REI: What’s the Difference?

A PREI (Professional Real Estate Inspector) has 4+ years of experience and can work independently. An REI (Real Estate Inspector) has less experience and must be supervised by a PREI. For complex DFW properties with foundation concerns, older systems, or non-standard construction, hiring a PREI is the safer choice. Always confirm the license type using TREC’s official license search before booking.

Continuing Education and Professional Credentials Beyond TREC Licensing

A TREC license establishes that an inspector has met Texas’s minimum professional standards. But minimum standards are exactly that — a floor, not a ceiling. The inspectors who consistently deliver the most thorough, accurate evaluations are typically those who pursue professional credentials and continuing education well beyond what TREC requires.

Two organizations set the standard for professional inspector credentials: the American Society of Home Inspectors (ASHI) and the International Association of Certified Home Inspectors (InterNACHI). Both require inspectors to pass rigorous examinations, adhere to strict codes of ethics, and maintain ongoing education requirements. When you see these credentials listed on an inspector’s profile, it’s a meaningful signal — not just marketing language.

Inspectors who hold professional inspector certifications from ASHI or InterNACHI have demonstrated a commitment to quality that goes beyond what the state requires. They’ve chosen to hold themselves to a higher standard — and that choice matters when you’re trusting someone to evaluate a $400,000 asset.

ASHI vs. InterNACHI: Understanding the Difference

The ASHI Certified Inspector (ACI) designation is widely considered one of the most rigorous in the industry. ASHI requires candidates to complete a minimum number of paid inspections, pass the National Home Inspector Examination (NHIE), and adhere to ASHI’s Standards of Practice and Code of Ethics. ASHI’s emphasis on in-field experience before certification means that ACI holders have typically conducted hundreds of real inspections before earning the credential.

The InterNACHI Certified Professional Inspector (CPI) designation takes a different but equally rigorous approach. InterNACHI offers an extensive library of online coursework covering every aspect of home inspection, from structural systems to specialty areas like thermal imaging and radon. CPI candidates must pass InterNACHI’s examination, adhere to their Code of Ethics, and complete ongoing annual continuing education. Many InterNACHI members also carry E&O insurance as a requirement of membership.

Both credentials are positive indicators. Neither is definitively “better” than the other — they reflect different educational philosophies, both aimed at producing competent, ethical inspectors. What matters most is that the inspector holds current membership (not just a lapsed credential) and actively participates in the continuing education requirements. When evaluating inspectors, ask specifically whether their ASHI or InterNACHI membership is current and active.

Why Continuing Education Keeps Inspectors — and Buyers — Protected

TREC requires 16 hours of continuing education annually for licensed inspectors, including mandatory legal and ethics courses. This baseline requirement ensures that inspectors stay current with regulatory changes and ethical standards. But the building industry evolves constantly — and 16 hours per year is a modest commitment for a profession where staying current directly affects the quality of the service delivered.

Building codes change. Texas has been updating its electrical standards in alignment with the National Electrical Code (NEC), and inspectors who aren’t current on these changes may miss code-related issues in newer construction. New construction techniques — spray foam insulation, advanced framing, engineered lumber — require updated knowledge to evaluate properly. Technology has also transformed inspection practice: thermal imaging cameras, moisture meters, drone-assisted roof inspections, and sewer scope cameras are now standard tools for thorough inspectors, and using them effectively requires training.

When you’re evaluating inspectors, ask about their recent continuing education. An inspector who can speak specifically about recent coursework — foundation evaluation techniques, thermal imaging interpretation, new construction defect patterns — is demonstrating active engagement with their profession. That engagement directly translates to better inspections and fewer missed defects.

Inspectors who invest in ASHI or InterNACHI certifications and ongoing training demonstrate a commitment to quality that protects you. If you want that level of professionalism for your DFW home purchase, Journey Home Inspections brings certified expertise to every inspection.

General Liability Insurance: The Often-Overlooked Protection

Most conversations about inspector insurance focus on E&O coverage — and for good reason. But there’s a second type of insurance that every professional inspector should carry, and it covers a completely different category of risk: General Liability (GL) insurance.

GL insurance covers third-party claims for bodily injury or property damage that occur during the course of the inspector’s business operations. If an inspector accidentally damages your property during the inspection — breaks a fixture, damages a roof component while evaluating it, or causes a water leak while testing plumbing — GL insurance covers the repair cost. If someone is injured on the property during the inspection, GL insurance covers the liability.

TREC does not mandate GL insurance for licensing purposes. But the absence of GL coverage is a meaningful gap in professional protection. Inspectors who carry comprehensive inspection coverage — both E&O and GL — are demonstrating a complete approach to professional risk management. GL premiums typically run $1,000–$2,500 annually, which is a modest cost relative to the protection it provides.

GL vs. E&O: What Each Policy Actually Covers

The distinction is straightforward once you understand the underlying risk each policy addresses:

General Liability insurance covers physical incidents — property damage or bodily injury caused by the inspector’s presence and activities on the property. Examples: an inspector’s ladder damages a gutter, a piece of equipment scratches hardwood floors, or a contractor trips over the inspector’s equipment and is injured. GL covers the resulting claims.

Errors & Omissions insurance covers professional failures — mistakes, oversights, or negligent omissions in the inspection report itself. Examples: failing to identify a visible foundation crack, missing signs of active roof leakage, or failing to report an electrical panel that poses a fire risk. E&O covers the financial consequences of these professional failures.

Both policies are essential for comprehensive professional protection. When you’re vetting inspectors, ask specifically whether they carry both types of coverage. An inspector who carries E&O but not GL has a gap in their professional insurance profile. An inspector who carries neither is operating without any meaningful financial accountability.

🏠 DFW-Specific Inspection Concerns

DFW’s clay soil and slab foundations create unique inspection challenges that require specific expertise. Look for inspectors with documented experience evaluating foundation movement, soil expansion patterns, and slab-related issues. This isn’t generic knowledge — it’s local expertise that directly affects the quality of your inspection report. For pier and beam foundation inspections, this specialized knowledge is even more critical.

DFW Market Context: Why Professional Standards Matter Here Specifically

The DFW metroplex is one of the fastest-growing regions in the country, with a population exceeding 8 million residents and residential construction continuing at a high pace across the region. This growth creates a robust market for home inspections — and a competitive landscape where the quality of inspectors varies significantly.

The DFW metro currently has an estimated 1,000–1,500+ active TREC-licensed inspectors. That’s a substantial supply, which gives buyers meaningful choice. But high supply doesn’t mean uniform quality. The range of experience, insurance coverage, and professional credentials across that pool is wide — and the consequences of choosing poorly can be severe.

For buyers purchasing home inspections in Fort Worth and surrounding areas — including Weatherford, Justin, Eagle Mountain, Roanoke, Southlake, and Trophy Club — understanding the local market context is essential to making a good hiring decision. This isn’t a one-size-fits-all market. Different parts of DFW have different housing stock, different soil conditions, and different inspection challenges.

DFW-Specific Inspection Challenges That Demand Expert Evaluation

Clay soil is the defining geological factor in DFW home inspections. The region’s expansive clay soil — sometimes called “black gumbo” — swells when wet and shrinks when dry, creating constant movement beneath slab foundations. This movement is gradual and cumulative. Over years, it can cause significant structural damage: sticking doors, cracked walls, uneven floors, and eventually, compromised structural integrity.

An inspector without specific experience evaluating DFW slab foundations may miss early warning signs of problematic movement. The difference between “normal settling” and “active foundation distress” requires trained eyes and local knowledge. This is one area where the PREI designation and local experience matter enormously — a generic inspection checklist isn’t sufficient for DFW’s specific soil conditions.

HVAC systems face extreme stress in North Texas. Summer temperatures regularly exceed 100°F, and air conditioning systems run continuously for months. An inspector evaluating a home in spring or fall may not be able to fully assess HVAC performance under peak load conditions — but a thorough inspector will note the system’s age, condition, and any visible signs of strain, and will clearly communicate the limitations of an off-season evaluation.

The mix of housing stock in DFW also creates inspection complexity. Older Fort Worth neighborhoods have homes with aging electrical systems, galvanized plumbing, and original roofing that require different evaluation approaches than the new construction in Weatherford, Justin, and Eagle Mountain. New construction phase inspections catch builder defects before they’re covered by drywall and finishes — a service that’s particularly valuable in DFW’s active new-construction market.

Market Growth and Inspector Supply in Suburban DFW

The rapid suburban expansion of DFW — into Parker County communities like Weatherford, Denton County areas like Justin and Argyle, and Tarrant County growth corridors like Eagle Mountain and Roanoke — has increased both inspection demand and the logistical challenges for inspectors. Tarrant County has approximately 300–400 active licensed inspectors. Parker County has roughly 50–75. Denton County has around 150–200.

This geographic distribution matters for scheduling. During peak transaction seasons — spring (March through May) and fall (September through November) — inspector availability in outer suburban areas can be limited. Planning ahead and booking inspections early is particularly important in these markets. The post-NAR settlement environment has also increased buyer reliance on thorough inspections, further tightening scheduling during peak periods.

The DFW metro sees an estimated 30,000–50,000+ home inspections annually based on transaction volume. That’s a significant market — and one where the stakes of a substandard inspection are high. With median home prices in the DFW area well above $350,000 in many submarkets, the financial exposure from a missed defect is substantial.

✅ It’s Smart to Verify Credentials — Here’s Why

You wouldn’t hire a contractor without checking their license. The same applies to home inspectors. Spending 10 minutes verifying TREC license status and checking for disciplinary actions can save you thousands in financial risk. The TREC license search tool is free, fast, and publicly available — use it every time.

Inspection Pricing and the Real Cost of Professional Insurance Coverage

Home inspection fees in DFW range from approximately $350 for smaller homes under 1,500 square feet to $900 or more for larger properties over 2,500 square feet. These fees reflect not just the inspector’s time — they reflect the full cost of operating a professional inspection business, including the insurance premiums that protect you as a buyer.

When you hire professional home inspection services with full insurance coverage, you’re paying for a comprehensive professional service that includes E&O insurance ($1,500–$5,000+ annually), General Liability insurance ($1,000–$2,500 annually), professional certifications and continuing education, specialized equipment, and detailed report generation. These are real operating costs that responsible inspectors build into their pricing — and they’re costs that uninsured inspectors avoid by passing the risk to you.

DFW inspection pricing runs approximately 10–20% higher than the national average, driven by higher demand in a booming market, increased insurance costs for Texas inspectors, and the prevalence of add-on services that buyers in this market have come to expect. That premium is justified — and it’s a small fraction of the financial exposure you’re managing.

Breaking Down What You’re Actually Paying For

The base inspection fee covers the inspector’s time on-site (typically 2–4 hours for an average DFW home), report generation (usually delivered within 24 hours), and the visual evaluation of all major systems required by TREC’s Standards of Practice. For most DFW homes, this is the foundation of a thorough inspection.

Add-on services increase the total cost but add significant value. A sewer scope inspection ($150–$350) uses a camera to evaluate the condition of the main sewer line — a service that’s particularly valuable in older DFW neighborhoods where cast iron or clay sewer pipes may be deteriorating. Thermal imaging ($100–$250) uses infrared technology to identify moisture intrusion, insulation gaps, and electrical hot spots that aren’t visible to the naked eye. Radon testing ($150–$300) measures radon gas levels, which can be elevated in some North Texas areas. Pool and spa inspections ($100–$250) evaluate the mechanical and structural condition of aquatic features — relevant for the many DFW homes with pools.

These add-ons aren’t upsells — they’re tools that provide information you genuinely need to make an informed purchase decision. An inspector who recommends a sewer scope on a 1970s Fort Worth home isn’t padding the bill; they’re protecting you from a potential $5,000–$15,000 sewer line replacement that wouldn’t show up in a standard visual inspection.

Insured vs. Uninsured: The Financial Risk in Plain Numbers

Let’s be direct about the financial math here, because it’s the clearest argument for hiring a properly insured inspector.

Scenario A: You hire an insured PREI for $650. The inspector carries $500,000 E&O coverage and $1,000,000 GL coverage. Three months after closing, you discover a foundation issue the inspector should have flagged. You file an E&O claim. The insurance company investigates, and you receive a settlement of $18,000 toward the $22,000 repair cost. Your net out-of-pocket: $4,000 plus the inspection fee.

Scenario B: You hire an uninsured inspector for $380. Three months after closing, you discover the same foundation issue. You have no E&O claim to file. You can attempt to sue the inspector personally, but they have no assets to pursue and the legal costs exceed any potential recovery. Your net out-of-pocket: $22,000 plus legal fees.

The $270 you saved in Scenario B cost you $22,000. This isn’t a worst-case hypothetical — it’s a pattern documented across Texas inspection liability cases. The financial case for hiring an insured inspector is overwhelming.

Red Flags: How to Spot Underinsured or Unprofessional Inspectors

The DFW inspection market’s size and competitiveness means that not every inspector advertising services is operating at the professional standard you deserve. Knowing what to look for — and what to avoid — is the practical skill that separates buyers who protect themselves from those who don’t.

The most important tool in your verification arsenal is TREC’s license search. Before booking any inspector, take two minutes to verify inspector credentials on TREC’s license search tool. Confirm the license is “Active,” note whether it’s PREI or REI, and check for any disciplinary actions. This single step eliminates a significant category of risk.

Questions to Ask Before Hiring Any Inspector

A professional inspector will answer these questions directly and without hesitation. Vague, evasive, or defensive responses are themselves red flags.

- “Are you a TREC-licensed PREI?” — Confirm the specific license type, not just that they’re “licensed.”

- “What is your E&O insurance coverage limit? Can you provide a certificate?” — Aim for $500,000 minimum per occurrence; $1,000,000 is better. Request the actual certificate, not just a verbal confirmation.

- “Do you carry General Liability insurance?” — Both GL and E&O should be in place.

- “Are you ASHI or InterNACHI certified, and is your membership current?” — Confirm current, active membership status.

- “What is the liability cap in your inspection agreement?” — Understand your maximum recovery before signing.

- “Do you have any disciplinary actions on your TREC license?” — A professional with a clean record will confirm this readily; you can verify independently through TREC.

- “What specific services are included in the base fee, and what are the add-on costs?” — Transparency about pricing reflects professional integrity.

Predatory Practices That Should End the Conversation

Some inspector behaviors aren’t just red flags — they’re disqualifying. If you encounter any of the following, walk away and find a different inspector.

Operating without a TREC license is illegal in Texas. Some individuals advertise “inspection services” without holding a valid TREC license. Always verify before booking — not after.

Claiming E&O coverage but refusing to provide documentation is a serious red flag. Any inspector who says “I have E&O insurance” but won’t provide a current certificate of insurance is either uninsured or carrying coverage they don’t want you to scrutinize. Either scenario is unacceptable.

Recommending specific contractors for repairs is a TREC violation when it involves referral fees or kickbacks. TREC Rule 535.156 prohibits inspectors from accepting compensation for contractor referrals. An inspector who consistently steers buyers toward a particular contractor should be viewed with suspicion — and reported to TREC if you have evidence of a financial arrangement.

Exaggerated guarantees — promises that the inspection is “guaranteed” or that you’ll be “fully protected” against any post-closing issues — are misleading. E&O insurance covers negligence within defined limits. No inspection can guarantee that every future problem will be caught. Inspectors who make sweeping guarantees are either misrepresenting their coverage or don’t understand it.

Pressure to book quickly without time to verify credentials is a manipulation tactic. A professional inspector will give you the time you need to verify their license, review their insurance documentation, and read their inspection agreement before committing. Urgency pressure is a sales tactic, not a professional practice.

Ready to hire an inspector who meets all professional standards and carries robust insurance? Journey Home Inspections offers comprehensive E&O and GL coverage, TREC PREI licensing, local DFW expertise, and transparent credentials — no pressure, no guesswork.

Consumer Recourse: What to Do If Your Inspector Misses a Major Defect

Even with the best intentions and a qualified inspector, inspections aren’t perfect. If you discover a significant defect after closing that you believe should have been caught during the inspection, you have several potential avenues for recourse — but understanding how each works is essential to pursuing the right path.

The TREC complaint process is one avenue, but it’s important to understand what TREC can and cannot do. TREC regulates licensing and enforces professional standards — it can investigate whether an inspector violated the Standards of Practice or other TREC rules. But TREC does not mediate financial disputes or award damages. Filing a TREC complaint can result in disciplinary action against the inspector, which protects future consumers, but it won’t put money in your pocket.

For financial recovery, your primary options are an E&O insurance claim, legal action under the Texas DTPA, or contractual negotiation. Understanding which path is appropriate depends on the specific facts of your situation.

Filing an E&O Insurance Claim: The Step-by-Step Process

If you believe an inspector’s negligence caused you financial harm, the E&O insurance claim process is typically the most direct path to recovery. Here’s how it works:

Step 1: Document everything. Gather the original inspection report, photographs of the defect, repair estimates from licensed contractors, and any expert assessments confirming that the defect was reasonably discoverable at the time of inspection. The strength of your claim depends on your ability to demonstrate that a competent inspector should have identified the issue.

Step 2: Contact the inspector. Before filing a formal claim, notify the inspector of the issue. Some disputes are resolved at this stage without formal insurance involvement. Document all communications in writing.

Step 3: File a claim with the E&O carrier. If direct resolution fails, contact the inspector’s E&O insurance carrier — the carrier name and contact information should be on the certificate of insurance you requested before hiring. Submit your documentation and a written description of the alleged negligence.

Step 4: Cooperate with the investigation. The insurance company will investigate the claim, potentially hiring independent experts to evaluate whether the defect was reasonably discoverable. This process takes time — typically weeks to months. Be patient and maintain thorough records throughout.

Step 5: Negotiate the settlement. If the claim is accepted, the insurance company will offer a settlement. Remember that the inspector’s contract liability cap may limit the maximum recovery, and the settlement will be within the policy limits. Consult with an attorney if the settlement offer seems inadequate relative to your documented damages.

TREC Enforcement vs. Financial Recovery: Understanding the Difference

Filing a TREC complaint and pursuing financial recovery are separate processes that serve different purposes. TREC enforcement protects future consumers by holding inspectors accountable to professional standards. Financial recovery — through E&O claims or legal action — addresses your specific financial loss.

TREC can impose fines, require additional education, suspend a license, or revoke a license entirely for serious violations. These are meaningful consequences that protect the profession’s integrity. But they don’t compensate you for a $25,000 foundation repair.

The Texas Deceptive Trade Practices Act (DTPA) provides an additional legal avenue if the inspector’s conduct involved deception or fraud — not just negligence. DTPA claims can result in treble damages (triple the actual damages) in cases of knowing violations. However, pursuing DTPA claims requires legal representation and can be time-consuming and expensive. Consult with a Texas consumer protection attorney if you believe your situation involves deceptive practices beyond simple professional negligence.

“The most important thing you can do to protect your recourse options is to verify insurance and read the contract before the inspection happens — not after. Once you’ve signed the agreement and the inspection is complete, your options are defined by the terms you agreed to.”

Top Home Inspectors in DFW: Compared and Reviewed

The DFW inspection market includes solo operators, multi-inspector firms, and national franchise operations — each with different strengths, pricing structures, and insurance profiles. Understanding how these categories compare helps you make a more informed decision based on your specific property, location, and priorities.

For a detailed side-by-side comparison of national franchise options, the local inspector vs. national franchise inspection service quality guide for DFW provides an in-depth analysis of the tradeoffs. Here’s a practical overview of the major categories.

Journey Home Inspections — Fort Worth, TX

Journey Home Inspections, based in Fort Worth, TX, is a locally owned inspection firm with deep roots in the Tarrant County, Parker County, and Denton County markets. As a TREC-licensed Professional Real Estate Inspector, Journey Home Inspections brings the experience and independence that complex DFW properties require.

What sets Journey Home Inspections apart in the DFW market is the combination of local expertise and comprehensive professional standards. The firm carries both E&O and General Liability insurance — not just the state minimum — and maintains professional certifications that reflect a commitment to ongoing education and quality. The team understands DFW’s specific inspection challenges: clay soil foundation movement, slab-specific issues, the demands of North Texas summers on HVAC systems, and the differences between evaluating a 1960s Fort Worth bungalow and a 2024 new construction in Weatherford.

Service offerings include comprehensive general home inspections, new construction phase inspections, pool and spa inspections, septic system inspections, pier and beam foundation inspections, thermal imaging, and detailed reporting. The firm serves buyers throughout Fort Worth, Weatherford, Justin, Eagle Mountain, Roanoke, Southlake, Westlake, Argyle, and Trophy Club — the full geographic range of DFW’s western and northern growth corridor.

For buyers who want to understand the firm’s track record before booking, the Journey Home Inspections reviews page provides verified client feedback. The FAQ page addresses common questions about the inspection process, pricing, and what to expect in your report.

National Franchise Providers: Pillar to Post, WIN Home Inspection, HouseMaster

National franchise inspection companies offer brand recognition and standardized training across their networks. Pillar to Post, WIN Home Inspection, and HouseMaster are the most prominent franchises operating in the DFW market, and they have genuine strengths worth acknowledging. For a detailed breakdown of how these franchises compare on pricing and service quality, the HouseMaster vs. Pillar to Post inspector reviews and pricing comparison provides useful context.

Franchise operations typically carry higher E&O limits — often $500,000 to $1,000,000 or more — due to corporate backing and standardized risk management requirements. Their reporting platforms are often technologically sophisticated, with consistent formatting and digital delivery. Training standards are established at the corporate level, providing a baseline of consistency across franchise locations.

The important caveat: franchise quality depends significantly on the individual operator running the local franchise. The corporate training and insurance standards are consistent, but the inspector conducting your inspection is a local business owner who may have varying levels of experience and local market knowledge. Always verify the individual inspector’s TREC license status and credentials — not just the franchise brand.

Franchise pricing may also be higher than local firms due to franchise overhead and royalty structures. This isn’t inherently a problem, but it’s worth evaluating whether the premium is justified by the specific inspector’s credentials and local expertise.

Solo Operators and Multi-Inspector Firms

Solo operators represent a significant portion of the DFW inspection market. Many are highly experienced PREI holders who have built strong local reputations through years of consistent, quality work. Solo operators often provide more personalized service — you’re working directly with the inspector who will conduct your inspection, not a dispatcher scheduling one of many team members.

The variability in this category is wider than with franchises or established local firms. E&O coverage among solo operators ranges from the TREC minimum ($100,000 per occurrence) to $500,000 or more. Some solo operators carry robust coverage and hold ASHI or InterNACHI certifications. Others carry minimum coverage and have no credentials beyond their TREC license. The verification process is the same regardless of business model: check the TREC license, request insurance documentation, and review the inspection agreement before signing.

Multi-inspector firms offer wider availability — particularly valuable during peak spring and fall seasons when solo operators may be booked out for weeks. These firms typically have more standardized reporting processes and may carry higher aggregate E&O limits due to the volume of inspections they conduct. The tradeoff is that you may not know which specific inspector will conduct your inspection until closer to the scheduled date.

Key Takeaways: Protecting Your Investment Through Professional Standards

Buying a home in DFW is a significant financial commitment — and the home inspection is one of the most important steps in protecting that investment. The professional standards and insurance requirements covered in this guide aren’t bureaucratic details. They’re the framework that determines whether you have meaningful financial protection when something goes wrong.

Here’s what to carry forward from everything we’ve covered:

- E&O insurance is your financial safety net — but coverage limits, policy exclusions, and contract liability caps all affect how much protection you actually have. Always request documentation, not just verbal confirmation.

- TREC licensing is mandatory — verify “Active” status and confirm PREI designation for the highest level of experience and independence. Use TREC’s official license search tool every time.

- ASHI and InterNACHI certifications signal quality beyond minimum standards — look for current, active membership, not just a credential listed on a website.

- General Liability insurance matters — both GL and E&O should be in place for comprehensive professional protection. Ask about both.

- DFW’s specific challenges require local expertise — clay soil, slab foundations, extreme summer heat, and a mix of housing stock demand inspectors who understand this market, not just generic inspection protocols.

- Cheaper isn’t better — the financial math is clear. Saving $200–$300 on an uninsured or underinsured inspector is not a rational tradeoff when the potential exposure is $10,000–$50,000+.

- Take time to evaluate thoroughly — DFW’s competitive market gives you options. Use them. Spend 30 minutes verifying credentials, reading the inspection agreement, and comparing two or three inspectors before committing.

For buyers in Fort Worth, Weatherford, Justin, Eagle Mountain, Roanoke, Southlake, and surrounding areas, professional home inspection services in DFW that meet all of these standards are available — you just need to know what to look for. Now you do.

Frequently Asked Questions About Property Inspector Liability Insurance and Professional Standards

What happens if my home inspector misses a major problem?

If a licensed inspector negligently misses a significant defect that was reasonably discoverable at the time of inspection, you may have grounds to file a claim with the inspector’s Errors & Omissions (E&O) insurance. The process involves documenting the missed defect with repair estimates and an expert assessment confirming the defect was visible and identifiable during the inspection. Your recovery is limited by the policy’s coverage limits and any liability cap stated in the inspection contract — which in many cases limits recovery to the inspection fee paid. Consulting with a Texas consumer protection attorney is advisable if the financial loss is significant.

Does Errors & Omissions (E&O) insurance actually pay out for missed defects?

Yes — E&O insurance is specifically designed to cover legal defense costs and settlements or judgments resulting from alleged negligence or errors in the professional inspection service. When a claim is substantiated, the insurance company covers defense costs and pays settlements up to the policy limit. However, it’s not a blanket guarantee of full repair cost recovery: policies have coverage limits (typically $100,000–$1,000,000), contain exclusions for genuinely hidden defects or items outside the TREC SOP scope, and the inspector’s contract may cap your recovery at the inspection fee itself. Understanding these limitations before hiring is essential.

Should I hire a TREC Professional Real Estate Inspector (PREI) or just a regular Real Estate Inspector (REI)?

For most DFW property purchases, hiring a PREI is the safer and more informed choice. A PREI has completed 360 hours of qualifying education, accumulated 4+ years of licensed inspection experience, passed the TREC examination, and can practice independently — meaning their professional judgment isn’t subject to oversight by a supervising inspector. An REI has less experience and must work under PREI supervision. For complex properties with foundation concerns, older systems, or non-standard construction — which describes a significant portion of DFW’s housing stock — the PREI’s additional experience directly translates to more thorough defect identification and more reliable professional accountability.

What’s the difference between General Liability and E&O insurance for home inspectors?

These two policies cover completely different categories of risk. General Liability (GL) insurance covers third-party claims for bodily injury or property damage caused by the inspector’s business operations — for example, if the inspector accidentally damages a fixture, scratches flooring with equipment, or if someone is injured during the inspection. Errors & Omissions (E&O) insurance covers claims related to professional failures in the inspection service itself — missed defects, inaccurate reporting, or failure to follow TREC’s Standards of Practice. Both are essential for comprehensive professional protection, and you should verify that your inspector carries both before booking.

How do I verify that an inspector is actually licensed and insured?

Verifying TREC license status takes about two minutes using the official license search at TREC’s license lookup tool. Search by the inspector’s name or license number, confirm the status shows “Active,” note whether the designation is PREI or REI, and check for any disciplinary actions listed. For insurance verification, request a current certificate of insurance — not just a verbal confirmation — showing the carrier name, policy dates, coverage limits for both E&O and GL, and the named insured. Any reputable, properly insured inspector will provide this documentation without hesitation. If an inspector is reluctant or evasive about sharing these documents, that reluctance is itself a red flag.

What can TREC do if my inspector did a bad job?

TREC has meaningful enforcement authority over licensed inspectors and can impose fines, require remedial education, suspend a license, or revoke a license entirely for serious or repeated violations of TREC rules and Standards of Practice. Filing a TREC complaint is an important step when an inspector has violated professional standards — it creates a record and can protect future buyers from the same inspector. However, TREC does not mediate financial disputes or award damages to individual complainants. For financial recovery, you need to pursue an E&O insurance claim against the inspector’s carrier or take legal action under the Texas Deceptive Trade Practices Act (DTPA) — two separate processes from the TREC complaint, and both may be appropriate to pursue simultaneously.

Your Home Deserves an Inspector Who’s Accountable to You

You’ve done the research. You understand what proper licensing looks like, what E&O insurance actually covers, and what questions to ask before signing an inspection agreement. Now it’s time to put that knowledge to work.

Journey Home Inspections serves buyers throughout Fort Worth, Weatherford, Justin, Eagle Mountain, Roanoke, Southlake, Westlake, Argyle, Trophy Club, and the broader DFW area — with TREC PREI licensing, comprehensive E&O and GL insurance, and the local expertise that DFW’s clay soil and slab foundations demand. We’re transparent about our credentials and happy to provide documentation before you book.